Banking Sector Dollarisation is Down, But High Risks Persist

The dollarisation of Uzbekistan’s banking sector remains one of the key topics closely followed by financial analysts and regulators alike. A high share of foreign-currency loans could give rise to serious risks, particularly in the SME segment. The previous article, published by Kursiv Uzbekistan, discussed banks’ asset quality. We now propose to take a closer look at the issue of dollarization, given some notable changes that have taken place over the past few years

What Do We Mean By Dollarisation

We define the dollarization of banking assets/liabilities as the share of assets/liabilities denominated in foreign currency to their total value (including assets/liabilities in local currency). In our credit analysis, we pay special attention to the dollarization of banks’ loan books as they typically comprise the bulk of their total assets.

High Loan Dollarisation Presents High Risks for Banks

Historical experience shows that high dollarisation levels in emerging markets, such as Uzbekistan, create heightened risks for banks, particularly weighing on their loan quality. Given these countries’ high dependence on volatile external economic conditions and lower stability of their financial systems compared to more developed countries, they are more vulnerable to the risk of significant weakening of their national currencies relative to the dollar and other global reserve currencies, which in extreme cases can take the form of a sharp devaluation.

Local-currency depreciation means the debt burden of those who borrowed in foreign currency increases, and the weaker the currency, the more it grows. As a result, borrowers find it harder to service their foreign currency loans, and some loans may become non-performing.

Worse still, if it happens to many retail borrowers, one could talk about risks to social stability. Take Kazakhstan: after the global financial crisis of 2008–2009 that triggered a series of sharp devaluations, many people could not pay off their foreign-currency mortgages, which banks had actively issued previously. Ultimately, the government had to step in and implement special refinancing programmes whereby mortgages were converted to local currency at a pre-devaluation rate. This is why multiple countries have introduced significant restrictions on the issuance of foreign-currency retail loans, which are completely banned in Uzbekistan.

Why, then, do borrowers in such countries are keen to take out loans in foreign currency? This is mainly because local currency interest rates are typically materially higher, given high inflation. Suppose the exchange rate is relatively stable, or there is only a slight weakening of the local currency (as we have observed in Uzbekistan in recent years). In that case, borrowers may deem it more beneficial to take on currency risk, hoping there will be no serious devaluation soon. Given the lower interest rate on the foreign-currency loan, they will save on interest payments. This may look like a reasonable strategy in the short term but may pose significant risks for both borrowers and banks in the long run.

Foreign currency liabilities Are Also Risky

The same logic largely explains high deposit dollarization in emerging markets. With high inflation and local currency depreciation, people and companies prefer to keep their savings and cash balances in more stable currencies. This results in a shortage of long-term stable funding in local currency in such countries, so banks are forced to fund their long-term lending with foreign currency liabilities.

Again, a significant weakening of the local currency gives rise to risks for banks. In this case, their liabilities to clients increase in local currency terms. Meanwhile, as discussed earlier, the quality of foreign-currency loans typically deteriorates, meaning that banks may receive lower interest income than expected. In the worst-case scenario, this can lead to serious liquidity risks. Risks increase further if loans are predominantly issued in local currency and are mainly funded by foreign currency liabilities. This may result in a substantial open currency position. In most emerging markets, FX risk hedging instruments are not developed, and closing such a position can be problematic.

Dollarisation in Uzbekistan is High…

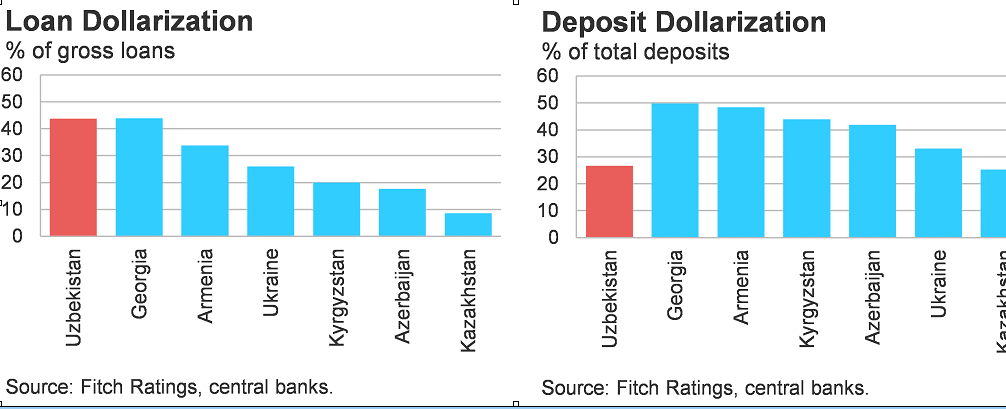

Among the post-Soviet countries for which Fitch Ratings provides bank rating coverage, Uzbekistan has one of the highest levels of loan dollarization – along with Georgia (foreign-currency loans accounted for 44% of gross loans in both countries in September 2024). However, there is a catch: some foreign-currency loans in Georgia are retail exposures (most notably foreign-currency mortgages), while all foreign-currency loans in Uzbekistan are issued to corporate borrowers and SMEs. Loan dollarization is significantly lower in other post-Soviet countries (especially in Kazakhstan, which is below 10%).

We consider this level of loan dollarization in Uzbekistan to be high, yet there are some nuances. In particular, the share of foreign-currency loans in large state-owned banks focused on lending to state-owned entities (SOEs) and the corporate sector is significantly higher than the sector average (over 60% for some banks). These are typically bulky foreign-currency loans issued to finance large infrastructure projects. Risks are mitigated through partial state funding and the availability of government guarantees on some loans.

Loan dollarization in other Uzbek banks is significantly lower (25% by September 2024, we estimate), and their foreign-currency loans are much less concentrated, as they are mainly issued to SMEs (which we still consider risky, as discussed above).

Regarding deposit dollarisation, Uzbekistan has one of the lowest ratios among the peer group, along with Kazakhstan (27% at end-September 2024). However, it should be noted that deposits have not yet become the predominant source of funding for banks in Uzbekistan (particularly for state-owned lenders), unlike in other post-Soviet countries. Large Uzbek state-owned banks remain dependent on external funding (mainly from foreign banks and international financial institutions), primarily in foreign currency loans. This, in effect, means that the actual dollarization of Uzbek banks’ liabilities is materially higher.

…But is Trending Down

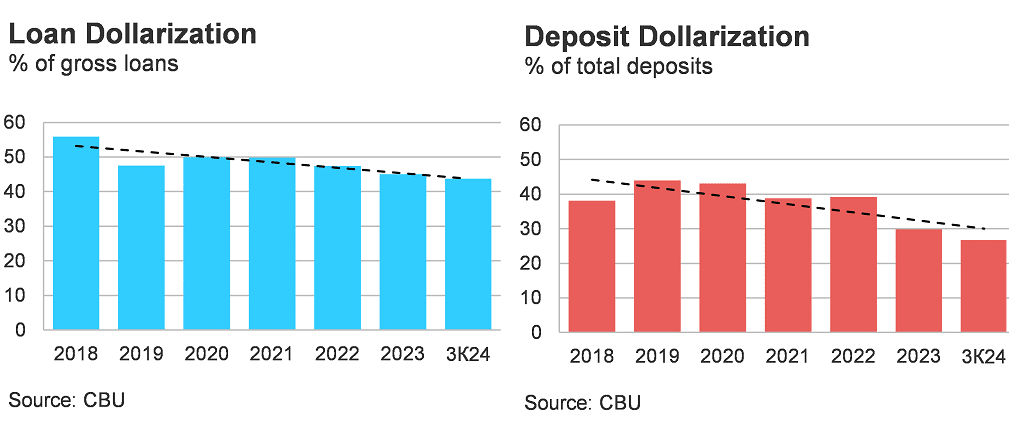

Over the past few years, we have noted a positive trend of gradually decreasing dollarization in the Uzbek banking sector. The share of foreign-currency loans in the system has been reduced by 12 percentage points since 2018, and 11 percentage points have reduced the share of foreign-currency deposits over the same period. These situational factors and objective reasons could explain this trend. An example of the former was the transfer of a large volume of foreign-currency SOE loans to the UFRD in 2019, which led to a sharp one-time decrease in loan dollarization; another was the partial conversion of some foreign-currency loans into soum. The main objective factor for de-dollarization has been the rapid retail lending growth over the past two to three years, denominated entirely in soum. The relative stability of the soum exchange rate and a more active adoption of banking services by businesses and the population have contributed to a higher share of soum deposits in banks.

De-Dollarisation Prospects

Should we expect a further decrease in dollarization levels in Uzbekistan’s banking sector going forward? We believe that this trend will continue in a stable economic environment, albeit gradually, so we would not anticipate a significant drop in the share of foreign-currency loans and obligations in Uzbek banks any time soon. The dynamics of corporate lending will be necessary. For example, if some large-scale investment projects were to be initiated, this would likely result in banks issuing large-ticket foreign-currency loans, which, in turn, would drive up loan dollarization. Conversely, continued rapid retail lending growth would lead to a lower share of foreign-currency loans.

However, the key factor that could affect the current de-dollarization trend is the dynamics of the soum exchange rate against the dollar. A more significant weakening of the national currency than in previous years would push dollarization levels in the banking sector higher.