Fitch: Uzbek Banks Received $2 Bn in State Support, But New Risks Emerge

Over the past five years, Uzbekistan’s state-owned banks have received approximately $2 bn in government support. However, they continue to face significant challenges, said Pavel Kaptel, Director of Fitch Ratings for the banking sector, during a conference in Tashkent on April 16. Among the major risks, he highlighted high levels of non-performing loans (NPLs), persistent dollarisation, and reliance on external financing.

Banking Reform: Ambitious Plans vs. Reality

For the past five years, Uzbekistan has undergone large-scale banking reforms to privatising state-owned banks, with support from the European Bank for Reconstruction and Development (EBRD) and other development institutions.

«The main success so far has been the privatisation of Ipoteka Bank, which was sold to the major international financial group OTP,» Kaptel noted.

However, he acknowledged that the privatisation of other large state-owned banks, originally scheduled for 2023–2024, has faced multiple delays. According to a presidential decree, the sale of controlling stakes in SQB, Asaka Bank, and Aloqabank is now planned for the end of 2025.

Fitch Ratings considers this a highly ambitious task. Pavel Kaptel noted that while efforts by the government, Central Bank, and the banks themselves have intensified, Fitch expects that selling all three banks this year will be difficult — likely, only one or two will be privatised later.

Sustainable foreign investor interest, especially amid global financial uncertainty, will be critical to the success of these sales.

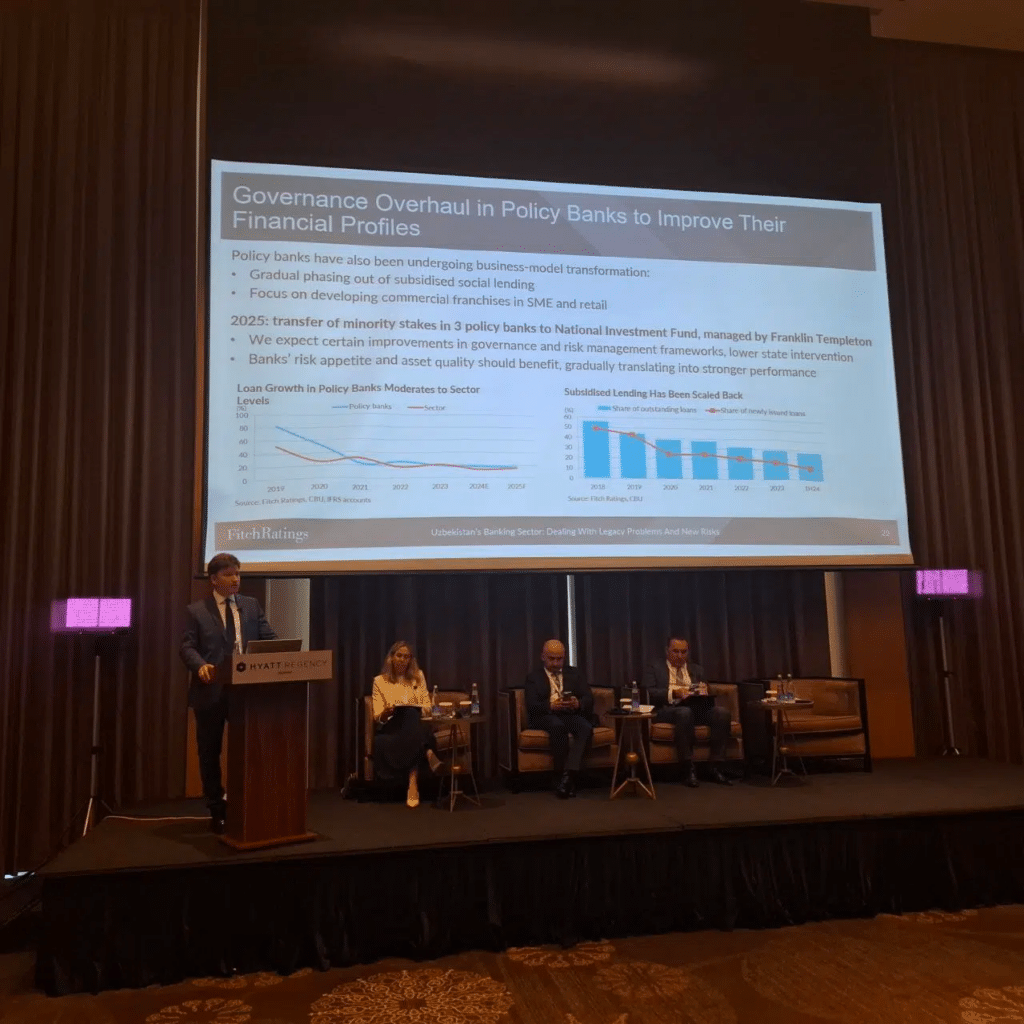

Another key reform element involves transforming state-owned banks focused on concessional lending to a more commercial model, particularly targeting small and medium-sized businesses (SMEs) and retail clients.

A major recent development is the creation of the National Investment Fund, which took over significant minority stakes in People’s Bank, Business Development Bank, and Microcreditbank. Management of the fund has been assigned to Franklin Templeton, a move Fitch believes will greatly improve the banks’ efficiency, governance, management quality, and risk management.

Structural Risks: Dollarisation and Asset Quality

Kaptel also pointed to long-standing structural risks in Uzbekistan’s banking sector.

Dollarisation remains high but is steadily declining. Central Bank data shows that foreign currency loans have dropped by 42% and deposits by 25%. However, these levels are still high compared to other CIS countries, posing risks to asset quality, especially given the limited infrastructure for currency risk hedging.

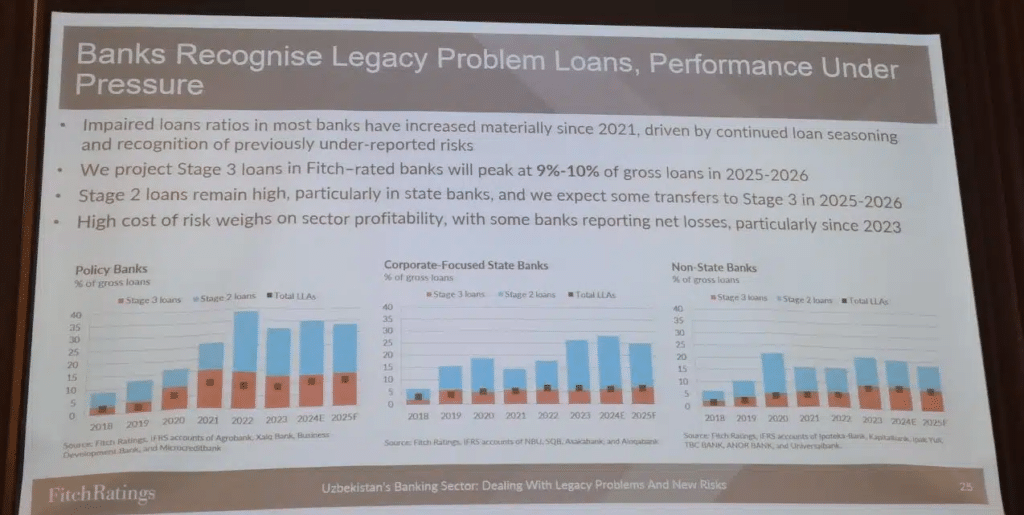

Another significant risk is asset quality deterioration, particularly in state-owned banks. This stems from the maturing of loans issued under weaker standards in previous years and stricter recognition of problem assets. Fitch forecasts that NPL ratios could peak at 9–10% of total loans (IFRS standards) in 2025–2026 before gradually declining.

Fitch categorises banks into three groups for asset quality analysis:

- State banks focused on concessional lending,

- Large state corporate banks,

- Non-state banks.

The first group has the highest NPL ratios, impacting profitability and sometimes leading to losses.

Government Support and External Financing Dependence

Over the past five years, state support for banks amounted to about $2 billion — around 2% of last year’s GDP. Most of the aid was directed toward banks specialising in concessional lending, while SQB and Asaka Bank received relatively less, aimed mainly at maintaining capital adequacy.

Uzbekistan is unique among post-Soviet countries in that nearly half of state bank liabilities are funded externally. Private banks, by contrast, rely primarily on deposits. Though most external funding comes from international institutions under favourable terms, and short-term refinancing risks are low, this dependence remains a structural risk.

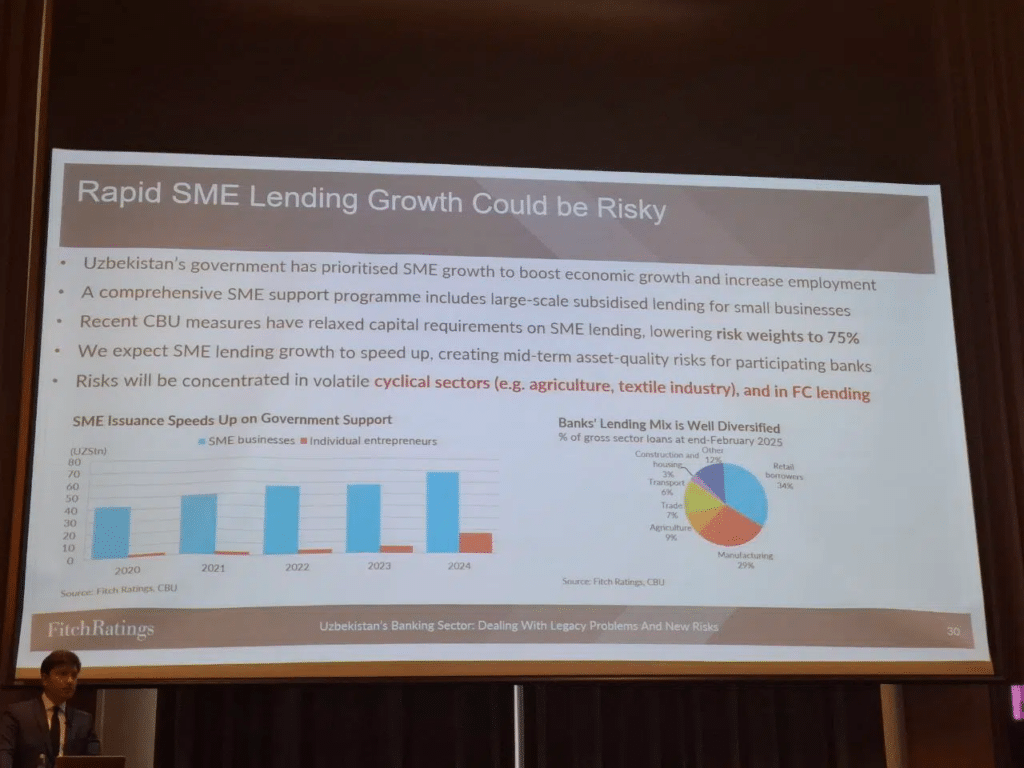

New Risks: Retail and SME Lending Booms

Kaptel also discussed emerging risks linked to the rapid expansion of retail and SME lending.

Retail lending, previously negligible, has grown at explosive rates, particularly in 2022–2023 (almost 50% year-over-year). While this reduces dollarisation and increases profitability, it risks overheating the consumer credit market — a trend observed in other post-Soviet economies.

The Central Bank has proactively introduced tight restrictions on high-risk retail lending segments. As a result, retail loan growth slowed significantly in 2024, particularly in auto loans and concessional family business loans, the riskiest areas, according to Fitch.

However, microloans and consumer loans continue growing rapidly, partly due to a low base effect. Fitch expects further Central Bank measures to curb risks, possibly including new restrictions on microloans.

In the SME segment, rapid credit growth poses similar concerns. The Business Development Bank has been designated to support this sector. Although the Central Bank recently relaxed capital requirements to boost SME lending, Fitch warns that excessive exposure could create risks, especially in cyclical sectors like agriculture, construction and textiles.

Currency risks are also high in SME loans, as many are denominated in foreign currencies without proper hedging, while only a few borrowers have export revenues.

Fitch will continue closely monitoring these segments in future banking sector reports.

Earlier, Kursiv Uzbekistan reported that in Uzbekistan, the factoring portfolio is projected to grow from 1.5 trillion soums in 2024 to over 10 trillion soums in 2025.