Central Asia’s Growth Outlook Strengthens to 3.4% in 2025, Says IMF

The International Monetary Fund (IMF) has revised upward its economic growth forecast for the Middle East and Central Asia region, now expecting a 3.4% expansion in 2025, up from 2.4% in 2024.

Projection for 2026 is slightly higher at 3.5%. The updated figures, released in the IMF’s July 2025 World Economic Outlook Update, reflect a broader global trend of tentative resilience, shaped largely by shifting trade policies, a softer US dollar, and improved financial conditions.

Global Context Supports Regional Momentum

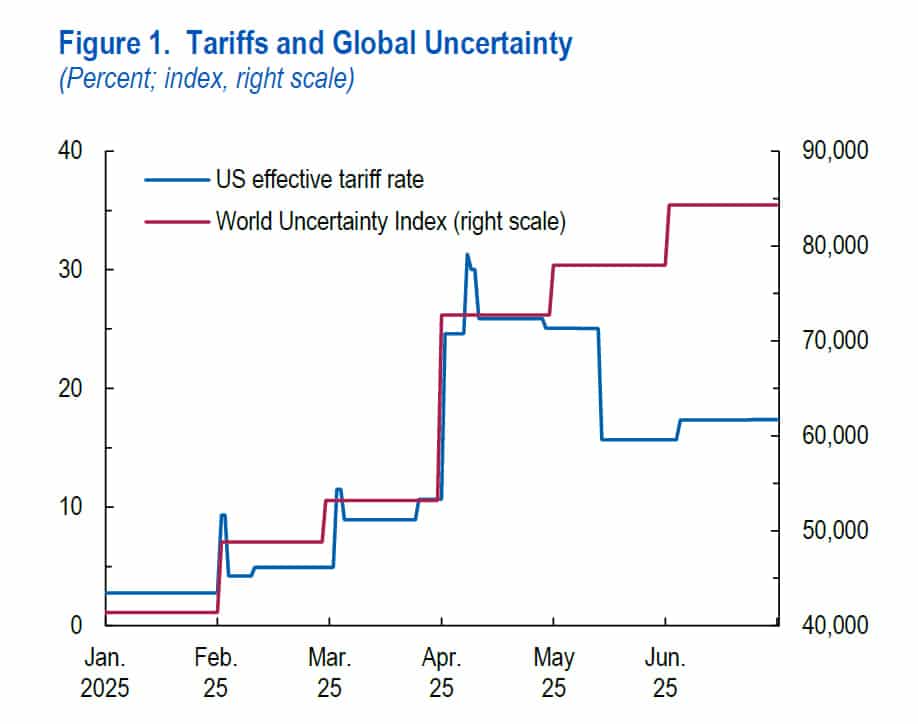

The IMF attributes part of the regional growth upgrade to wider global developments, particularly the unexpected easing of trade tensions and the temporary lowering of tariffs by the United States and China. The weakening of the US dollar has allowed more monetary flexibility for emerging markets, while rising business investment and trade have contributed to stronger-than-expected global output in early 2025.

Although global growth is expected to slow slightly, from 3.3% in 2024 to 3.0% in 2025, the deceleration is viewed as a return to more typical rates rather than a signal of instability. For Central Asia, the IMF’s optimism also stems from improving domestic conditions and policy responses in several countries.

Broad-Based Growth Across Central Asia

All five Central Asian states — Uzbekistan, Kazakhstan, Kyrgyzstan, Tajikistan and Turkmenistan — are set to benefit from stronger global trade, fiscal expansion, and a weaker US dollar, which is easing pressure on external debt and inflation.

Kazakhstan, the region’s largest economy, is forecast to grow by 5.0% in 2025, the strongest among its neighbours. Its energy sector, investment projects and relative fiscal discipline are driving the upward trend.

Uzbekistan is projected to maintain solid growth momentum, supported by continued investment in infrastructure, state reforms, and expanding trade ties. While the IMF did not publish a specific figure for Uzbekistan in this update, its outlook aligns with the region’s improving trend.

Kyrgyzstan and Tajikistan are likely to benefit from increased remittances and trade, particularly with Russia and China. Fiscal support and higher gold and aluminium exports continue to play a stabilising role.

Turkmenistan, although less integrated globally, is seeing stronger gas exports and moderate recovery in domestic demand.

Growth Across the Broader Region

The IMF’s broader classification of the Middle East and Central Asia region also includes oil-exporting and importing economies beyond Central Asia. Saudi Arabia’s economy is forecast to rebound sharply, with growth reaching 3.6% in 2025 and 3.9% in 2026, reflecting both energy price stabilisation and expanded fiscal spending.

In contrast, Russia, categorised under Emerging and Developing Europe, is expected to see growth drop to 0.9% in 2025, down from 4.3% in 2024, following tighter trade restrictions and higher tariffs on critical exports. This slowdown could indirectly impact some Central Asian trade corridors and remittance flows.

Trade and Tariff Shifts Create Short-Term Gains

The IMF highlights that much of the current growth momentum stems from «front-loading» of trade activity in anticipation of higher future tariffs. In the first half of 2025, firms globally increased imports and investments to get ahead of expected trade costs. This temporary surge has benefited export-oriented economies, including those in Central Asia.

However, the report cautions that this dynamic could reverse in 2026 as the short-term boost fades. Even so, medium-term prospects for the region remain steady, with structural reforms, infrastructure projects, and improved fiscal management playing a role in maintaining growth.

Inflation and Monetary Space

Inflation in emerging markets and developing economies is projected to decline to 5.4% in 2025 and 4.5% in 2026, providing scope for some Central Asian countries to ease monetary policy. Lower energy prices and subdued domestic demand are expected to further reduce inflationary pressure.

The IMF also notes that the weakening dollar has helped reduce pressure on local currencies and debt servicing costs in countries with high external borrowing.

Policy Priorities for Stability

The report urges governments in the region to continue focusing on prudent fiscal management, targeted support measures, and structural reforms to build resilience against future shocks. It also highlights the importance of international cooperation and trade diversification in light of ongoing geopolitical and economic uncertainty.

With downside risks still present, from a potential rise in tariffs to renewed geopolitical tensions, the IMF underscores the need for contingency planning and clear communication from policymakers.