Asset Quality: Key Challenge for Uzbekistan’s Banking Sector

Fitch Ratings currently provides analytical coverage for fifteen banks in the Republic of Uzbekistan, including all the largest lenders. As of 1 September 2024, Fitch-rated banks accounted for 84% of total sector assets, 86% of sector loans, and 79% of sector deposits. In our view, there are some issues in Uzbekistan’s banking sector that may impact the banks’ credit profiles and their ratings. Asset quality is of higher importance, so we would like to discuss it first.

Key Metric

According to our Bank Rating Criteria, analyzing asset quality (and particularly loan quality) is one of the critical parts of credit rating work as asset quality has a material impact on other aspects of banks’ credit profiles. If problem assets increase substantially, banks have to create additional loan loss reserves, which affects their profitability and, in turn, weighs on their capitalisation. Conversely, sustainably good asset quality through the cycle tends to result in stable performance and high capital ratios.

How to Assess Asset Quality

There are a number of financial ratios that can help assess banks’ asset quality, but the key ratio is the share of problem, or impaired, loans in their total loan books. However, there is a catch: there is no single definition for problem loans. National regulators (including the CBU) usually define them as so-called non-performing loans, or NPLs. These are loan exposures that are overdue for more than 90 days. According to the CBU’s latest data, the sector-average NPL ratio was equal to 4.2% as of 1 September 2024, up from 3.5% at 1 January.

In our credit analysis, we do not view the NPL ratio as the key metric in assessing banks’ asset quality as it only captures problem loans based on formal quantitative criteria. In our view, a more accurate ratio is the share of loans classified as Stage 3 loans under IFRS 9. This accounting standard prescribes banks to classify all their loan exposures into one of three brackets, or Stages, based on their expected credit losses. As such, Stage 3 loans comprise not only regulatory NPLs but also other problem exposures – for example, those that are less than 90 days overdue or restructured loans that would have otherwise become impaired.

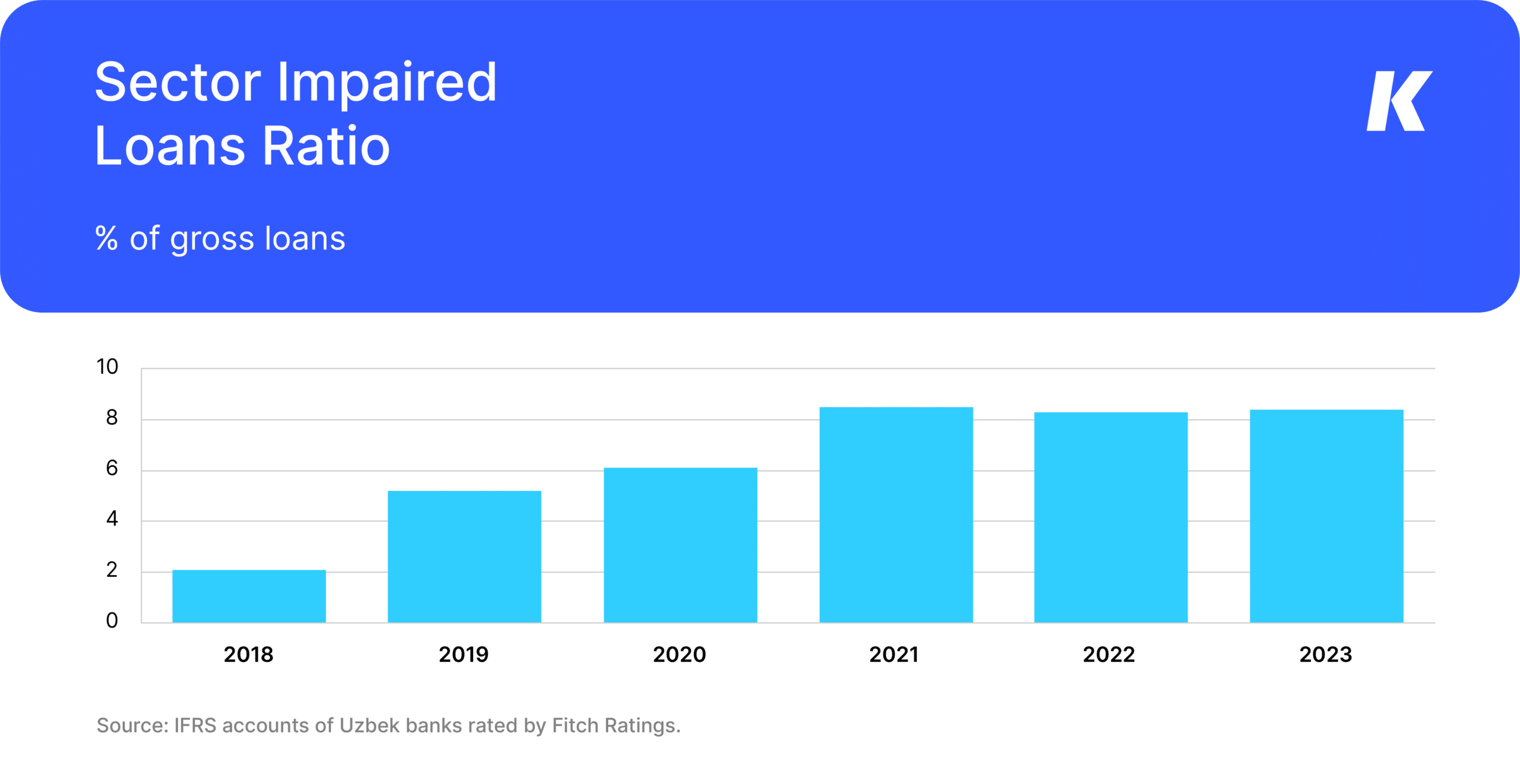

Problem Loans on the Rise: What’s Going On?

The share of problem loans in Uzbekistan’s banking sector has been on a sustainably upward trend in recent years. For Fitch-rated banks, the average Stage 3 loans ratio has increased materially from 2021 and has stabilised in the 8%-9% range over the past three years, roughly twice as high as the regulatory NPL ratio.

This build-up of problem exposures in the banking sector is primarily driven by two factors, in our view. Firstly, it has to do with seasoning of loans issued during the rapid loan expansion in 2018-2020, which was stimulated by high pent-up investment demand in the country. Over the past two to three years, grace periods on these loans have come to an end, and some borrowers have found it difficult to service their debt obligations (partly due to the negative effect of the pandemic and other adverse external events). In addition, we believe that underwriting standards in many banks (particularly state-owned lenders) were weak at the time and this also resulted in the accumulation of bad loans in their portfolios.

In our view, material deterioration of banks’ reported asset quality metrics is also, somewhat counter-intuitively, the result of their strengthened risk management frameworks, namely more conservative loan classification policies. We believe some of the local banks previously did not classify all their problem loan exposures into Stage 3, so the reported sector-average impaired loans ratio did not capture the amount of problems to the full extent. Since the banking sector reform began in 2020, the situation has significantly improved and banks’ reported impaired loans ratios give a more fair indication of the actual amounts of bad loans.

Diverging Trends

While the overall trend of weakening asset quality in the sector is evident, there is some divergence between individual banks. We note that loan quality dynamics have been the worst in a number of state-owned banks, particularly banks providing subsidised lending under government development programmes. Reported Stage 3 loans ratios in some of these policy banks have been more than double the sector-average levels, leading to high loan impairment charges and net losses. Loan quality in larger corporate-focused state banks has been more stable, while impaired loans ratios in private banks have typically been below the sector average.

Risky Segments

Our assessment of Uzbek banks’ asset quality considers their risk profiles, e.g. the share of loans in higher-risk industries in their total portfolios. In our view, subsidised development loans, including family business loans, bear the highest credit risk for banks. Such loans have accounted for a large portion of non-performing loans in some state-owned banks in recent years, as discussed above.

We also consider foreign-currency loans to local SME borrowers to be risky. A large portion of these loans were issued to clients that had limited hard-currency revenues (or none at all), which makes banks exposed to currency risks given the de-facto absence of hedging instruments on the local market and consistent, albeit moderate, depreciation of the local currency.

Some retail loans, particularly car loans and unsecured consumer loans, which grew rapidly in 2022-2023, carry higher credit risks. However, after the CBU introduced a host of restrictive measures, new loan issuance in these segments has materially decreased, which reduced risks of overheating, in our view.

What’s Next?

We believe that asset-quality metrics in Uzbekistan’s banking sector should stabilise in 2024-2025. According to our baseline scenario, the Stage 3 loans ratio could reach a peak of 9%-10% and then gradually start to trend down. Potential improvements in banks’ loan quality would likely be driven by substantial improvements in their underwriting standards over the last two to three years, banks writing off legacy problem exposures, and continued lending growth. Nonetheless, our forecast could be revised due to the potential impact of external factors and developments in the banking sector (e.g. privatisation of state-owned banks and CBU’s regulatory initiatives).

In addition, banks’ asset quality may be sensitive to FX rate movements given still high loan dollarisation in Uzbekistan. However, we believe this important topic is worth a separate discussion.