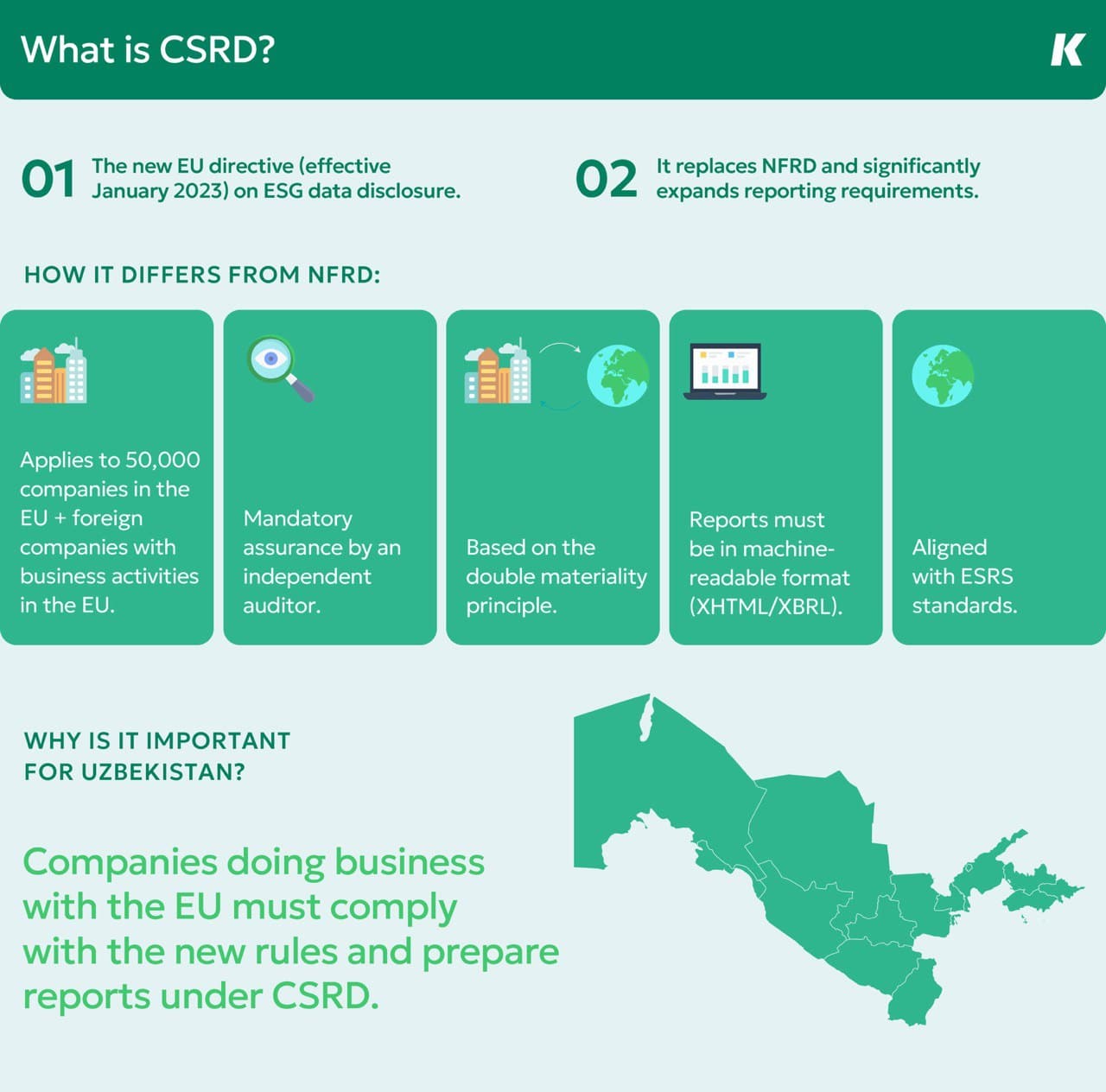

CSRD and Uzbekistan: How EU’s New Standards Are Changing Rules of Game for Business

Uzbekistan has set itself the target of achieving carbon neutrality by 2060. To this end, the country is expanding renewable energy, cutting emissions and introducing decarbonisation measures across key industries. These priorities are closely linked to international sustainability reporting standards — in particular, the EU’s Corporate Sustainability Reporting Directive (CSRD), which came into force in 2023.

By 2024, the EU ranked among Uzbekistan’s top three trading partners. For local businesses, compliance with CSRD is no longer just a matter of reputation but a prerequisite for access to the European market — especially in agriculture, textiles, chemicals and metallurgy.

At the core of CSRD is the European Sustainability Reporting Standards (ESRS) — a practical framework comprising two cross-cutting standards and ten thematic standards covering environmental, social and governance (ESG) issues. Disclosures are structured across four pillars: strategy, governance, risks and opportunities, and metrics with targets.

The ESRS have been designed in alignment with the IFRS Sustainability Disclosure Standards and GRI. This enables companies to build on existing data-collection processes while allowing investors to compare information across firms, even when they use different frameworks.

How ESRS differ from voluntary frameworks

Unlike voluntary ESG reporting, ESRS requirements are detailed, mandatory and include quantitative metrics with prescribed methodologies. Selective disclosure is not permitted. Data must be audited and integrated into financial reporting.

For Uzbekistan, this matters because the EU is one of its key trading partners. Adherence to CSRD/ESRS directly influences access to the European market and participation in supply chains.

CSRD and Uzbekistan’s climate strategy

Uzbekistan joined the Paris Agreement in 2017. In 2021, the country raised its climate ambition in its updated Nationally Determined Contribution (NDC): instead of the 10% reduction in greenhouse gas emissions intensity per unit of GDP (from 2010 levels) set in its first NDC, it now targets a 35% reduction by 2030.

CSRD supports these commitments by requiring:

- Reporting of Scope 1, 2 and 3 emissions, enabling companies to measure and cut their carbon footprint;

- Climate risk assessments, factoring in droughts, water scarcity and extreme temperatures across Central Asia;

- Decarbonisation planning, including roadmaps for renewable energy transition and improved energy efficiency.

In 2024, UzAssets published a roadmap on embedding sustainability principles into state-owned enterprises, followed by updated guidance in 2025. The document requires companies to carry out a double materiality assessment in 2025–2026 in line with ESRS 1 and 2 (General Requirements, General Disclosures). These standards define how businesses analyse both their impacts on society and the environment, and how external factors affect their financial position and outlook.

The complexity of CSRD and ESRS lies in their breadth — covering issues from climate to social impact. Unlike voluntary frameworks, the directive enforces standardised, mandatory rules. This reduces the risk of greenwashing and ensures comparability of data.

Why this matters for business and markets

Reporting in a machine-readable format (XHTML/XBRL) allows automatic integration of corporate data into international databases, making it readily accessible to all market participants. For investors, this is a risk and opportunity assessment tool; for consumers, a source of reliable information; for regulators, a mechanism to monitor sustainable development.

For businesses themselves, CSRD compliance strengthens reputation, improves risk management and enhances strategic planning. Meanwhile, regulators are working on interoperability between ESRS, IFRS SDS and GRI. This will reduce the reporting burden by allowing companies to meet multiple frameworks simultaneously.

How CSRD could affect businesses in Uzbekistan

Even companies not directly under EU jurisdiction may still be affected by CSRD — through supply chain obligations, investor and lender requirements, or voluntary adoption of standards to build reputation and enter new markets.

Supply chains are particularly critical. European firms must disclose ESG data and require the same from their partners. For Uzbek exporters, this is effectively a condition for doing business.

For example, a large textile holding in Uzbekistan supplies products to Poland, Latvia and Lithuania. European clients request data on CO₂ emissions, water consumption reduction, raw material traceability and social standards. Without such disclosures, the company risks losing contracts.

This trend has intensified with agreements between Uzbekistan and the EU. In 2024, the two sides signed a Memorandum of Understanding on sustainable raw material supply chains under the Global Gateway initiative. While this opens the door to investment, it also makes ESG compliance essential for businesses.

Another pathway is voluntary adoption. Some international firms are already applying ESRS to boost investor trust and prepare for stricter rules ahead. For Uzbek businesses, partial adoption can be a strategic step — helping build internal sustainability practices, manage climate and social risks, and establish robust data collection processes. Pilot implementation reduces risks and eases adaptation without deadline pressure.

Finally, multinational groups with EU subsidiaries must consolidate sustainability data across the whole group. This means their Uzbek entities will inevitably be drawn into CSRD reporting.

Recommendations for Uzbek companies preparing ESRS disclosures

As regulatory and international partner expectations rise, companies in Uzbekistan should prepare proactively.

Transparency is equally important. Companies must establish sustainability reporting processes in international formats, including machine-readable versions.

In practice, building an internal working group is advisable. This should include a sustainability coordinator, CFO, environmental specialist, HR manager, lawyer, IT analyst, as well as heads of logistics, production and procurement. Such a team can address ESRS 1 and 2, as well as thematic areas ranging from climate change, pollution and water management to biodiversity, social policy and business ethics.

Capacity-building is crucial. Staff should be trained in international reporting standards. Surveys can help segment training by role — managers, procurement staff, HR, accountants, technical teams.

At the early stages, engaging an external CSRD/ESRS consultant can speed up the process, cut costs and help avoid common pitfalls.