China Slows Down: Who Will Lead the Second Wave of the Electric Vehicle Boom

The global electric vehicle market is going through a period that seemed unlikely just a few years ago. China, which accounted for the majority of global EV sales growth, is gradually becoming a mature market, Europe is once again stimulating demand through subsidies, and the United States risks slowing its pace of electrification due to changes in regulatory policy. The new growth engines are emerging economies, from Turkey and Vietnam to Brazil and Indonesia.

According to BloombergNEF’s forecast, electric vehicles will account for 27% of the global passenger car market in 2026, with sales exceeding 23 mln units. Behind these record-breaking figures lies an important trend: the industry is shifting from rapid demand expansion to a struggle over manufacturing capacity, localization, and control of supply chains.

China Is No Longer the Main Growth Driver

Over the past five years, the state of the global electric vehicle market has largely been determined by one question: «What’s happening in China?» In 2025, the country accounted for 63% of global EV sales.

However, growth is slowing. BloombergNEF expects EV sales in China to increase by only 10% in 2026, compared with 16% a year earlier and 39% in 2024.

This trend points to the saturation of the world’s largest EV market. Demand remains high nearly 64% of all new vehicles sold in China this year will be electric, but the potential for exponential growth has largely been exhausted.

The saturation of the domestic market is pushing BYD, Geely, Chery and other Chinese companies to expand abroad. However, experts doubt that export activity alone will be able to offset the imbalance between production capacity and sustainable domestic demand.

Emerging Markets Become the New Battleground

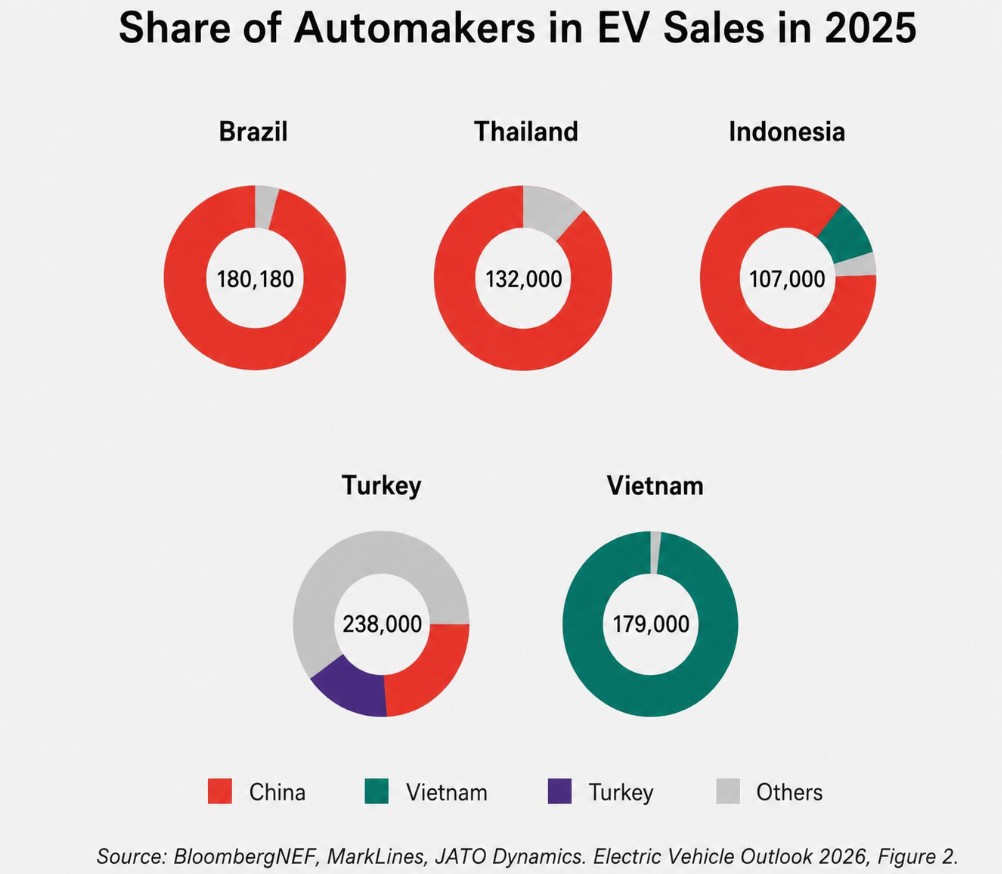

The fastest growth in electric vehicle adoption is no longer taking place in Western Europe or North America. In Turkey, EV sales more than doubled over the past year, rising from 108,000 to 238,000 vehicles. Their market share reached 22%.

In Vietnam, electric vehicles accounted for about 39% of new car sales, while in Singapore they approached the 50% mark. Indonesia has achieved a higher EV penetration rate than the United States, while Brazil and Mexico have already surpassed Japan.

China’s role varies significantly across these markets. Chinese brands control 96% of Brazil’s EV market and 88% of Thailand’s.

However, in Vietnam, nearly the entire market is driven by local manufacturer VinFast, while in Turkey, national automaker Togg remains one of the leading players.

These examples demonstrate that a high level of electrification does not necessarily require complete dependence on Chinese suppliers. Government support, tax incentives, and the development of domestic manufacturing can create a competitive industry even in countries with relatively small domestic markets.

Production Matters More Than Technology

Just a few years ago, the competitiveness of EV manufacturers was determined primarily by battery technology and software capabilities. Today, industry analysts increasingly point to another factor: manufacturing localization.

Experts at Strategy& conclude that locating assembly facilities close to the end market has become the most important tool for price competition. Import tariffs, transportation costs, tax differences, and trade restrictions can eliminate the advantages of low-cost manufacturing.

Take the BYD Seal U, for example. Despite its relatively low production cost in China, once European tariffs and other expenses are taken into account, the vehicle’s price in Germany becomes more than twice as high as it is on the Chinese domestic market.

The growing emphasis on localization presents governments with a new dilemma. On the one hand, protective measures support domestic manufacturers; on the other, they limit price competition and may slow EV adoption.

As Chinese investment in overseas manufacturing facilities continues to grow, finding the right balance will become one of the key challenges of industrial policy.

Europe Returns to Growth Through Subsidies

Despite concerns about weakening demand, the European electric vehicle market is showing signs of recovery.

In the first quarter of 2026, sales of fully electric vehicles in Europe’s five largest markets increased by 36% compared with the same period a year earlier. Growth reached 50% in France and 41% in Germany.

However, this rebound has been closely linked to the reinstatement of consumer support programs. Analysts note that the European market remains highly sensitive to changes in government policy. This suggests that electric vehicles have not yet achieved full independence from incentive measures.

At the same time, the gradual decline in battery costs is expected to further narrow the price gap between electric and gasoline-powered vehicles.

The United States Risks Losing Ground

The most challenging situation is unfolding in the United States. For the second consecutive year, BloombergNEF has downgraded its forecasts for EV adoption in the country.

Following the rollback of some support measures established under the Inflation Reduction Act, analysts expect U.S. EV sales to decline by 19% in 2026. Automakers are being forced to revise investment plans and postpone the launch of new models.

Just a few years ago, the U.S. market was seen as one of the key centers of global transport electrification. The current situation demonstrates how heavily the industry’s development depends on a stable regulatory environment.