Uzbekistan’s Export Paradox

President Mirziyoyev’s modernisation agenda delivered on trade infrastructure. The second chapter of reform, getting firms to actually use it, has barely begun. Credit where it is due. Uzbekistan’s trade reformers have done something genuinely impressive. In a region where border bureaucracy is measured in days and sometimes weeks, Uzbekistan has built a customs clearance process that takes just over two days on average, faster than the regional benchmark, faster than the global average and dramatically faster than Kazakhstan, whose firms wait nearly six times as long. Export compliance costs are lower than the global norm. In terms of the pure mechanics of moving goods across a border, Uzbekistan is a success story.

The puzzle is that the success story has not fully translated into exports. The World Bank’s 2024 Enterprise Survey finds that only a tiny fraction of Uzbek firms export at a meaningful scale, fewer even than the global average for lower-middle-income economies. The reform program worked. However, the results it was supposed to generate have not materialised. Understanding why is not just an academic exercise; it is the central question of Uzbekistan’s next phase of economic development.

Trade facilitation is not enough

The international development community spent much of the 2000s and 2010s focused on trade facilitation, reducing customs delays, harmonising documentation and digitising border procedures. The logic was straightforward: lower the cost of crossing the border and more firms will cross it. Uzbekistan absorbed this lesson and acted on it, and the clearance times speak for themselves. But a growing body of evidence, including the pattern now visible in Uzbekistan’s own data, suggests that logistics efficiency is a necessary but insufficient condition for export growth.

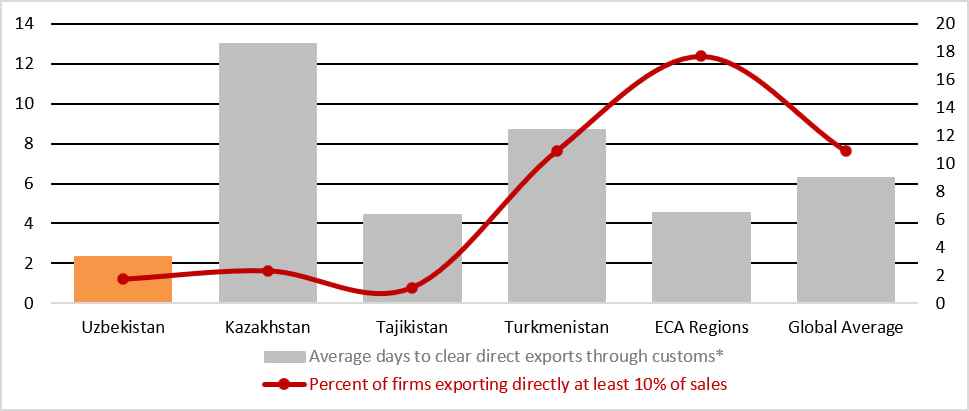

Customs clearance speed vs. export participation rate

Uzbekistan clears customs faster than every comparator, yet its firms export at the lowest rate in the region. The gap between logistics performance and export engagement is the defining feature of Uzbekistan’s trade profile.

What the logistics reforms cannot provide is a buyer. They cannot provide market intelligence about which products meet which standards in which countries. They cannot provide the pre-shipment working capital that allows a firm to produce an export order before receiving payment. They cannot provide the networks of agents, distributors, and quality certifiers that any exporter needs to navigate an unfamiliar market. These are the missing links, conspicuously absent from Uzbekistan’s current reform architecture.

Two numbers policymakers cannot ignore

Two data points from the survey deserve to be printed and framed in every relevant institution. First, firms with significant foreign investment export at rates nearly five times those of domestic firms, even though both groups face the same customs procedures and regulatory environment. This means the reforms have been most successful for the firms that needed them least, multinationals and joint ventures that would have found ways to export anyway. The domestic private sector, where the potential for broad-based growth lies, has been largely untouched.

Second: among firms that have actually exported, the perceived severity of trade constraints is lower than among non-exporters. This is the opposite of what you would expect if the system were genuinely difficult. It suggests that the barrier is not in the process itself, but in the knowledge that the process is navigable. Uzbekistan has reached a point where a significant portion of its export deficit may now be corrected through information, rather than further regulatory reforms. That is both a sobering finding and an encouraging one, because it implies that the most powerful intervention might also be among the cheapest.

Building the architecture of export growth

Uzbekistan’s revised Strategy 2030 sets clear numerical ambitions: GDP increasing to $240 bn, exports reaching $67 bn and the exporter base expanding to 15,000 firms. Targets of this scale, however, require more than aspiration; they require architecture.

What should the next phase of Uzbekistan’s trade reform look like? The data points toward a clear agenda. Export promotion must move from passive website maintenance to active buyer-matching, diplomatic missions turned into commercial intelligence posts, trade attaches with sector expertise and bilateral agreements that create preferential access for Uzbek goods in target markets. The Export Promotion Agency needs a budget, mandate, and accountability framework that match the ambition of the logistics infrastructure now behind it.

Trade finance is equally critical. The working capital gap that prevents small and medium firms from taking on export orders is not a market failure that will self-correct. It requires deliberate policy instruments: export credit guarantees, pre-shipment finance facilities through the state development bank, and currency hedging tools that protect firms against exchange-rate risk in international contracts. Several of Uzbekistan’s peer economies, such as Vietnam, Morocco, and Georgia, have built these instruments and seen measurable results in export diversification.

Untapped services export potential

There is one dimension of the reform agenda that has received a little attention but deserves far more: services exports. The survey data reveal that Uzbekistan’s services sector barely exports at all, a near-total absence that represents a significant missed opportunity given the country’s growing IT sector, its universities, and its tourism and cultural assets. Services trade requires a different policy toolkit than goods trade; it has nothing to do with customs clearance times and it is precisely the kind of high-value, knowledge-intensive export activity that could accelerate Uzbekistan’s path toward upper-middle-income status.

President Mirziyoyev has made economic modernisation a key goal of his administration. Much progress has already been made in building infrastructure. The next challenge is more difficult: strengthening institutions, developing firms and markets, expanding knowledge and gradually building a strong export culture. The facilities and systems are ready; now the real work begins.